Published: 24th May, 2026

Last Edited: 24th May, 2026

Buying your first flat is exciting and terrifying in roughly equal measure.

The excitement is obvious — you’re done with landlords, you’re building something real. The terrifying part is that nobody clearly explains the process. Everyone assumes you already know what a sale deed is, what stamp duty actually costs, and why the builder is asking for a booking amount before you’ve even seen the flat properly.

This guide changes that.

Every step below is written for someone buying their first flat in Goregaon — East or West — with real numbers from this specific market.

Step 1 — Figure out your real budget before you look at a single flat

This is where most first-time buyers make their first mistake.

They look at a ₹1.90 crore flat, see that their home loan covers ₹1.52 crore, and assume they need ₹38 lakh. The actual number is closer to ₹55–60 lakh.

Here’s why.

Add to the property cost: stamp duty (5–7%), registration (1%), GST on under-construction (1–5%), society deposit, interior costs, and moving expenses. The total all-in cost is typically 10–15% above the base property price. Jeff Lenney

Let’s make this real with a Goregaon example.

You’re buying a 2 BHK in Bangur Nagar, Goregaon West for ₹1.90 crore.

- Stamp duty at 6% (Mumbai rate with metro cess): ₹11.4 lakh

- Registration: capped at ₹30,000

- GST (if under-construction): 5% = ₹9.5 lakh

- Society maintenance deposit: ₹1–2 lakh

- Interior and basic furnishing: ₹4–8 lakh

- Shifting and miscellaneous: ₹50,000–₹1 lakh

Total all-in cost: approximately ₹2.18–₹2.25 crore

Your down payment (20% of loan value) plus these costs is the actual cash you need to have ready before the bank steps in.

Work this number out first. Then start looking at flats.

For a full stamp duty breakdown with Goregaon-specific examples, see: Stamp Duty in Mumbai 2026 — Exactly How Much Will You Pay? →

Step 2 — Understand what home loan you actually qualify for

Banks typically lend 75–80% of the property value. You fund the remaining 20–25% as a down payment.

Most banks require salaried applicants to earn at least ₹25,000 monthly. A CIBIL score of 725 or higher significantly boosts approval chances. Banks also want salaried applicants to show 2–3 years of work experience. NoBroker

The practical rule: your home loan EMI should not exceed 30–45% of your net monthly take-home salary. Jeff Lenney

Again — real Goregaon numbers:

If your monthly take-home is ₹1.2 lakh: Maximum comfortable EMI: ₹40,000–₹54,000/month At 8.75% interest over 20 years, this supports a loan of approximately ₹42–₹55 lakh

That means a ₹1.90 crore flat requires a ₹38 lakh down payment plus ₹25–28 lakh in buying costs. Total cash needed: ₹63–₹66 lakh.

If your monthly take-home is ₹2 lakh: Maximum comfortable EMI: ₹65,000–₹85,000/month This supports a loan of approximately ₹70–₹90 lakh

The fastest way to increase your eligible loan amount: Add a co-applicant — your spouse or a working family member. Co-applicants can combine incomes, and they’ll need to provide their own KYC and income documents. This is the most common strategy first-time buyers in Goregaon use to qualify for the flat they actually want. NoBroker

Check your CIBIL score before applying. It’s free once a year. If it’s below 700, spend 6 months clearing any outstanding dues before approaching a bank.

For a complete guide on this, see: Home Loan Eligibility for a Flat in Goregaon — How Much Can You Actually Borrow? →

Step 3 — Decide: Goregaon East or West, and which pocket

Now that you know your budget, it’s time to pick your market.

If your budget is ₹1.60–₹1.90 crore: In Goregaon West, look at Ram Mandir and Siddharth Nagar — resale 2 BHKs are available in this range. In Goregaon East, Jay Prakash Nagar and Pandurang Wadi have options in this bracket.

If your budget is ₹1.90–₹2.30 crore: In Goregaon West, Bangur Nagar and Shastri Nagar give you mid-range gated societies with full amenities. In Goregaon East, mainstream Gokuldham resale and newer projects in Dindoshi are your territory.

If your budget is ₹2.30 crore and above: Oshiwara and the Link Road belt in West. Dindoshi premium and Gokuldham newer projects in East.

Key lifestyle filter questions to ask yourself: Do you work in an IT park or on Film City Road? East is closer. Do you commute to Andheri or BKC daily? West’s Metro Line 2A is faster. Do you have children in school? Gokuldham’s school cluster in East is hard to beat. Do you want the mall, restaurants, and urban buzz right outside? West wins.

See the full comparison: Goregaon East vs Goregaon West — Which Side Should You Actually Live On? →

Inorbit Mall. Located on the Malad-Goregaon Link Road, Inorbit is one of the largest malls in western Mumbai. Inorbit Mall single-handedly transformed a once-quiet stretch into a real estate hotspot — property prices in the Link Road belt have increased four-fold since its opening. Houssed

Oberoi Mall. Situated on the Western Express Highway, Oberoi Mall attracts families and young professionals and has elevated the entire area’s lifestyle quotient significantly. Houssed

Motilal Nagar Redevelopment. The ₹36,000 crore Motilal Nagar redevelopment by Adani Group is set to create a modern township spanning 143 acres — one of the largest urban redevelopment projects in all of western Mumbai. It’s actively underway. Houssed

These three things are what put Goregaon West on people’s radar. If you’re moving here, they’re also what you’ll be living near.

Read our blogs and make your homebuying journey easier.

- All Posts

- Mumbai Real Estate

- Back

- Buyer's Guide

- Property Rates 2026

- 3BHK In Goregaon West

- 2BHK in Goregaon West

- Motilal Nagar Redevelopment

- Back

- Buyer's Guide

- Property Rates 2026

- 3BHK in Goregaon East

- Gokuldham Colony

- Back

- Buyer's Guide

- Goregaon West

- Goregaon East

- Goregaon East vs Goregaon West

- Property Stamp Duty & Registration Charges in Mumbai

- Check MahaRERA Registration

- Buyer's Guide

- Property Rates 2026

- 3BHK In Goregaon West

- 2BHK in Goregaon West

- Motilal Nagar Redevelopment

- Buyer's Guide

- Property Rates 2026

- 3BHK in Goregaon East

- Gokuldham Colony

- Back

- Property Stamp Duty & Registration Charges in Mumbai

- Check MahaRERA Registration

Step 4 — Start shortlisting: new project or resale?

Once you’ve picked your pocket, you need to decide what type of property to buy.

New / under-construction project:

The Upside: Modern layouts, new amenities, payment in stages (construction-linked plan).

The Downside: you wait 2–3 years for possession and pay both EMI and rent during that period. GST of 5% applies on under-construction purchases.

Ready-to-move resale flat:

The Upside: No GST (straight saving of 5%), immediate possession, and you can see the exact flat — not just a sample unit — before buying.

The downside: older building design, possibly higher maintenance, and less flexibility on customisation.

The honest financial logic for a first-time buyer in Goregaon:

If you’re currently renting in Mumbai, you’re paying rent every month. If you buy under-construction, you pay rent AND EMI for 2–3 years. That’s a real cash outflow of ₹40,000–₹60,000 rent plus ₹50,000–₹80,000 EMI simultaneously.

Ready-to-move eliminates that double burden from day one.

For a deeper breakdown: Ready to Move vs Under Construction Flats in Goregaon — Which Makes More Financial Sense in 2026? →

Step 5 — Visit the flat and ask the right questions

You’ve shortlisted 3–5 options. Now visit each one.

When you visit, don’t just look at the flat. Look at:

The building entrance and lobby. Is it maintained? Does the security guard know who’s coming in? Is the lift working and clean? These small signals tell you everything about the society’s management.

The floor and direction of the flat. Higher floors cost more but get better ventilation and less noise. Ask which direction the flat faces — cross-ventilation matters significantly in Mumbai’s humidity.

The carpet area, physically. Walk the rooms. Does the master bedroom comfortably fit a king bed plus wardrobe? Is the kitchen functional? A 650 sq ft flat on paper can feel spacious or cramped depending entirely on how the space is designed.

The society’s active issues. Talk to a resident, not just the seller or broker. Ask casually: “How’s the society committee? Any ongoing disputes? How’s the water supply?” Residents will tell you things the broker won’t.

Parking. Is your parking spot covered? Where is it? How many visitors can park? This sounds minor until you come home after a 10-hour day and spend 20 minutes finding space.

Step 6 — Verify the property before paying anything

This step happens before the booking amount. Not after.

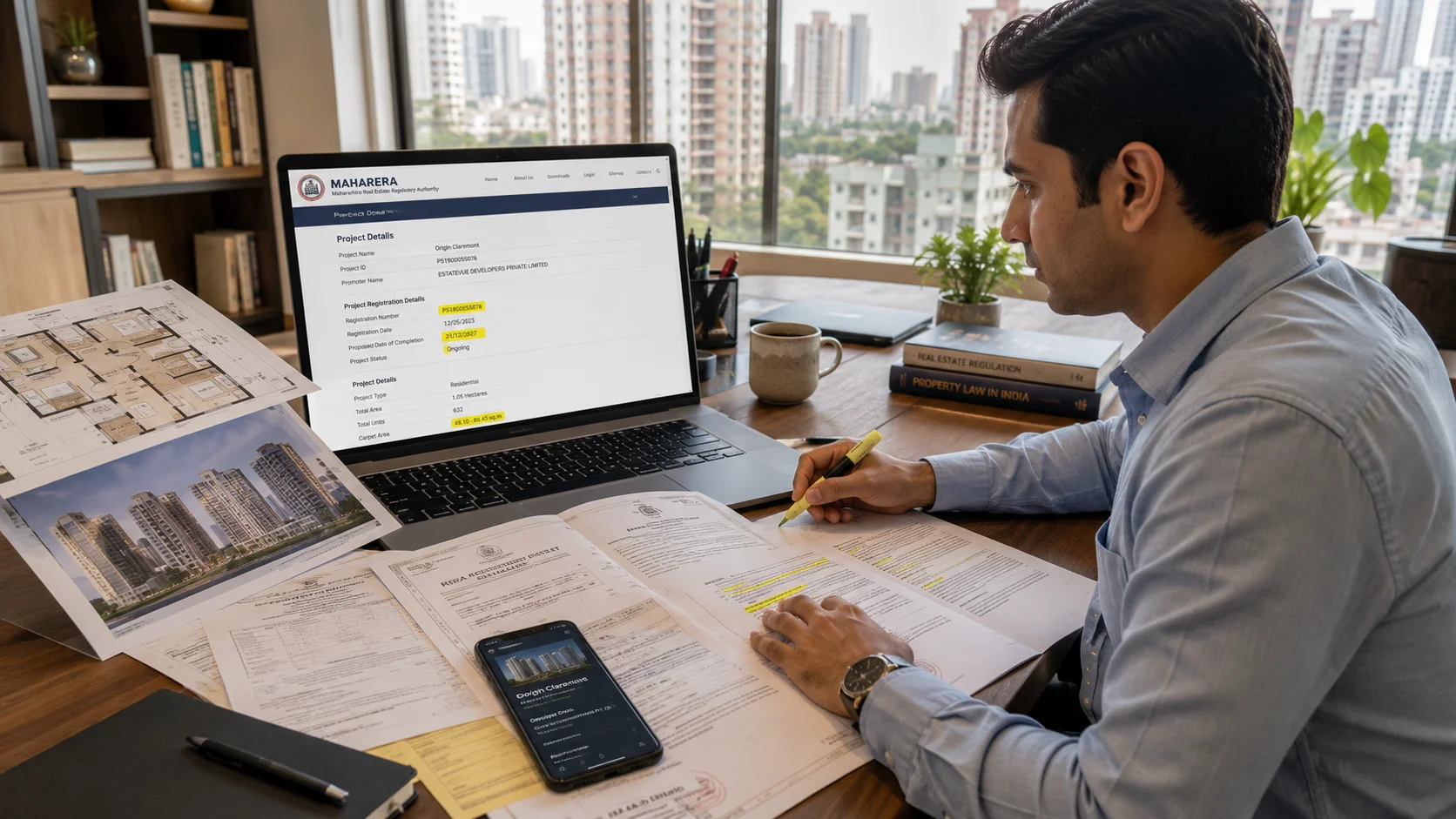

Check MahaRERA registration. Every new or under-construction project must be registered at maharera.mahaonline.gov.in. Check the respective RERA registration status of the property via the official portal. The entry shows the registered carpet area, possession date, and the builder’s compliance history. If the project isn’t registered, walk away. The DeltaNET

Check the title deed. The title deed confirms who legally owns the property and whether they have the right to sell it. A clear title is arguably the most important item among the documents to check before buying a flat in Mumbai, because every other agreement depends on it. Luxury Presence

Check the OC for resale flats. The Occupancy Certificate confirms the building is legally fit for habitation. The most important documents required for buying a flat are the Title Deed, the Agreement for Sale, the RERA registration certificate, the Occupancy Certificate, the Commencement Certificate, and the Encumbrance Certificate. No OC means the flat is technically illegal to occupy, and home loans are difficult to get on such properties. Luxury Presence

Check if the bank has approved the project. Before committing to a specific flat in Goregaon, check whether your preferred bank has already independently approved the project. HDFC, SBI, ICICI, and Axis Bank all publish approved project lists. A bank-approved project means the documents have already been independently verified — which saves you time and gives you confidence.

For a complete document verification checklist, see: What to Check Before Signing a Builder Agreement in Goregaon →

Step 7 — Pay the booking amount and sign the agreement

You’ve verified everything. You’re ready to move forward.

Booking amount: Typically 1–2% of the property value. On a ₹1.90 crore flat in Goregaon West, that’s ₹1.9–₹3.8 lakh. This amount is usually adjustable against the final purchase price. Get a receipt and ensure the booking is linked to a written offer letter.

Agreement for Sale: This is the formal document that outlines every term — the agreed price, payment schedule, possession date, penalty clauses for builder delay, carpet area, and amenities promised. Once the sale agreement is finalised, pay stamp duty via the GRAS portal and register the sale deed at the Sub-Registrar office. Jeff Lenney

Read this document fully. Not just the highlighted parts the broker shows you. Every clause matters — especially the penalty clause if possession is delayed (standard under RERA is interest at SBI’s lending rate), and the clause about what happens if the promised amenities aren’t delivered.

If anything is unclear, spend ₹5,000–₹10,000 on a property lawyer to review the agreement. It’s the cheapest insurance you’ll ever buy.

Step 8 — Apply for your home loan

Once the agreement is signed, apply for your home loan.

Documents required include KYC documents (Aadhaar, PAN, passport), proof of income (salary slips, ITRs), bank statements, and property documents such as the sale deed and NOC. NoBroker

The practical checklist for salaried buyers:

- Last 3 months’ salary slips

- Last 2 years’ ITR (Income Tax Returns)

- Last 6 months’ bank statements

- Form 16 from employer

- PAN card and Aadhaar card

- Property documents — agreement for sale, RERA certificate, title deed

Apply to 2–3 banks simultaneously. Don’t apply to 10 — every application creates a hard inquiry on your CIBIL and can slightly reduce your score. Two or three is the right number to compare offers without damaging your credit profile.

Most banks process home loans for approved projects in Goregaon within 7–15 working days if your documents are in order.

Step 9 — Pay stamp duty and register the property

This is the step that makes you the legal owner.

Stamp duty in Mumbai is 5% of the Agreement Value (or Ready Reckoner Value, whichever is higher), plus 1% Metro Cess — totalling 6%. Registration is 1% of the value, capped at ₹30,000. 99acres

On a ₹1.90 crore flat in Goregaon:

- Stamp duty at 6%: ₹11.4 lakh

- Registration: ₹30,000 (capped)

- Total: ₹11.7 lakh

If the flat is registered in a woman’s name, there is a 1% stamp duty rebate — but there is a catch: the flat cannot be sold for 15 years, or the saved amount must be repaid. For first-time buyers planning to hold long-term, registering in a woman co-owner’s name is a meaningful saving. 99acres

How the registration actually works in 2026:

As of 2026, the process is a hybrid of digital preparation and a brief physical visit for biometric verification at the Sub-Registrar’s Office (SRO). Enter property, buyer, seller, and witness details on the IGR Maharashtra Portal. Receive a PDE Token Number for appointment booking. Pay stamp duty and registration fees through the Government Receipt Accounting System (GRAS). Kolte-Patil

By law, registration must be completed within 4 months of signing the sale agreement. Missing this window can lead to penalties or even restarting the process. Kolte-Patil

The entire registration process typically takes 1–3 working days. Jeff Lenney

For the complete stamp duty calculation guide: Stamp Duty in Mumbai 2026 — Exactly How Much Will You Pay? →

Step 10 — Do your possession inspection before accepting the keys

The builder calls you for possession. Don’t go and sign on the same day.

Visit the flat first with a checklist. Walk through every room and note:

Walls and ceiling: Any seepage marks, cracks, or paint peeling? These are signs of structural issues or poor waterproofing.

Flooring: Check for chips, uneven tiles, or hollow-sounding spots (tap the tile — a hollow sound means poor adhesion).

Doors and windows: Open and close every single door and window. Do they fit properly without scraping? Are the frames properly sealed?

Electrical: Switch every light on and off. Test every socket with a phone charger. Check the MCB board.

Plumbing: Turn on every tap and flush every toilet. Check for drips, weak pressure, and drainage speed.

Parking spot: Physically verify the parking spot assigned to you matches the one mentioned in the agreement.

Obtain the Occupancy Certificate copy from the developer at possession. If the builder cannot provide an OC, do not sign the possession letter. Taking possession without an OC creates legal complications that are difficult and expensive to resolve later. Jeff Lenney

If you find issues — and most first-time buyers do — give the builder a written snag list. RERA requires builders to rectify defects reported within 5 years of possession at no additional cost.

The total buying timeline — what to expect

| Stage | Timeline |

|---|---|

| Budget calculation and pre-approval | 2–4 weeks |

| Property search and shortlisting | 4–8 weeks |

| Due diligence and document verification | 1–2 weeks |

| Booking amount and agreement | 1 week |

| Home loan processing | 2–3 weeks |

| Stamp duty payment and registration | 1–3 working days |

| Total (ready-to-move) | 2.5 to 4 months |

| Total (under-construction) | Above plus 2–3 years for possession |

The real costs summary — Goregaon 2 BHK at ₹1.90 crore

| Cost Item | Amount |

|---|---|

| Property price | ₹1,90,00,000 |

| Down payment (20%) | ₹38,00,000 |

| Stamp duty (6%) | ₹11,40,000 |

| Registration | ₹30,000 |

| GST (if under-construction at 5%) | ₹9,50,000 |

| Society maintenance deposit | ₹1,50,000 |

| Interior / furnishing (basic) | ₹5,00,000 |

| Legal / documentation fees | ₹50,000 |

| Total cash required | ₹66,20,000 |

| Home loan required | ₹1,52,00,000 |

These are illustrative estimates. Actual costs will vary based on the specific property, negotiation, and interior choices.

The single most important thing a first-time buyer in Goregaon needs to know

Don’t let urgency override verification.

Brokers will tell you “three other buyers are interested.” Builders will tell you “this price is only available this weekend.” Friends will tell you “property only goes up, just buy something.”

None of these are reasons to skip due diligence.

A flat in Goregaon is a ₹1.80–₹2.50 crore decision. The 10 days you spend verifying documents, checking RERA, and reading the agreement carefully are the cheapest 10 days of your entire homeownership journey.

Everything else — the commute, the views, the amenities — can be adjusted. A legal problem with the property cannot.

Buying your first flat in Goregaon and want help navigating the process?

Tell us your budget, preferred area, and where you are in your search — we'll help you shortlist the right options and guide you through every step. No brokerage from our side.

We usually respond within a few hours. No spam, no pressure

People also ask about buying a flat in Goregaon for the first time

What documents do I need to buy a flat in Goregaon?

The most important documents required for buying a flat are the Title Deed, the Agreement for Sale, the RERA registration certificate, the Occupancy Certificate, the Commencement Certificate, and the Encumbrance Certificate. As a buyer, you also need to provide your PAN card, Aadhaar card, passport-size photographs, and income documents for the home loan. For resale flats, additionally obtain the previous chain of sale agreements going back to the original builder-to-first-buyer agreement, and the society’s No Objection Certificate. Luxury Presence

How much down payment do I need to buy a flat in Goregaon?

Banks finance 75–80% of the property value. You fund the remaining 20–25% as down payment. On a ₹1.90 crore 2 BHK in Goregaon West, the down payment alone is ₹38–47.5 lakh. Add stamp duty (₹11.4 lakh), registration (₹30,000), and other costs, and the total cash you need before the bank steps in is approximately ₹55–66 lakh. Always calculate your total all-in cost — not just the down payment — before committing to a budget.

What is stamp duty on a flat in Goregaon in 2026?

Stamp duty in Mumbai is 5% plus 1% Metro Cess, totalling 6% of the Agreement Value or Ready Reckoner Rate, whichever is higher. Registration is 1% capped at ₹30,000. On a ₹1.90 crore flat, that’s ₹11.4 lakh in stamp duty plus ₹30,000 registration. If the flat is registered in a woman’s name, a 1% stamp duty rebate applies — saving ₹1.9 lakh — but the flat cannot be sold for 15 years without repaying the saved amount. See the full guide: Stamp Duty in Mumbai 2026 → 99acres

Do I pay GST on a flat in Goregaon?

Only on under-construction properties. GST of 5% applies to under-construction flat purchases. Ready-to-move flats with an Occupancy Certificate attract zero GST. On a ₹1.90 crore under-construction flat, that’s ₹9.5 lakh extra. This is one of the strongest financial arguments for buying ready-to-move in Goregaon, where the resale inventory is deep and well-priced. For more: GST on Under Construction Flats in Mumbai 2026 →

How do I verify if a builder in Goregaon is RERA registered?

Visit maharera.mahaonline.gov.in. Search by project name or the builder’s name. The MahaRERA entry will show the project’s registered carpet area, promised possession date, and the builder’s compliance history — including whether they’ve been penalised for delays on past projects. Seek the respective RERA registration status of the property via the official portal before paying any amount. If a builder in Goregaon resists giving you their RERA number, that resistance is your answer. For a complete walkthrough: How to Check RERA Registration of a Builder in Maharashtra → The DeltaNET

Is it better to buy in Goregaon East or West as a first-time buyer?

For most first-time buyers, Goregaon West offers slightly easier navigation — a deeper resale market with more inventory in the ₹1.65–₹2.10 crore range, and strong metro connectivity for a wide range of commutes. Goregaon East is the better choice if you work in an IT park, prioritise green space, or specifically want Gokuldham’s community environment. The full comparison — including price, appreciation, lifestyle, and commute — is here: Goregaon East vs Goregaon West — Which Side Should You Actually Live On? →

Explore more:

- 2 BHK Flats in Goregaon West — Prices, Localities, and Buyer’s Guide 2026 →

- 2 BHK Flats in Goregaon East — Localities, Prices, and What to Expect →

- Stamp Duty in Mumbai 2026 — Exactly How Much Will You Pay? →

- Home Loan Eligibility for a Flat in Goregaon — How Much Can You Borrow? →

- What to Check Before Signing a Builder Agreement in Goregaon →

- How to Check RERA Registration of a Builder in Maharashtra →